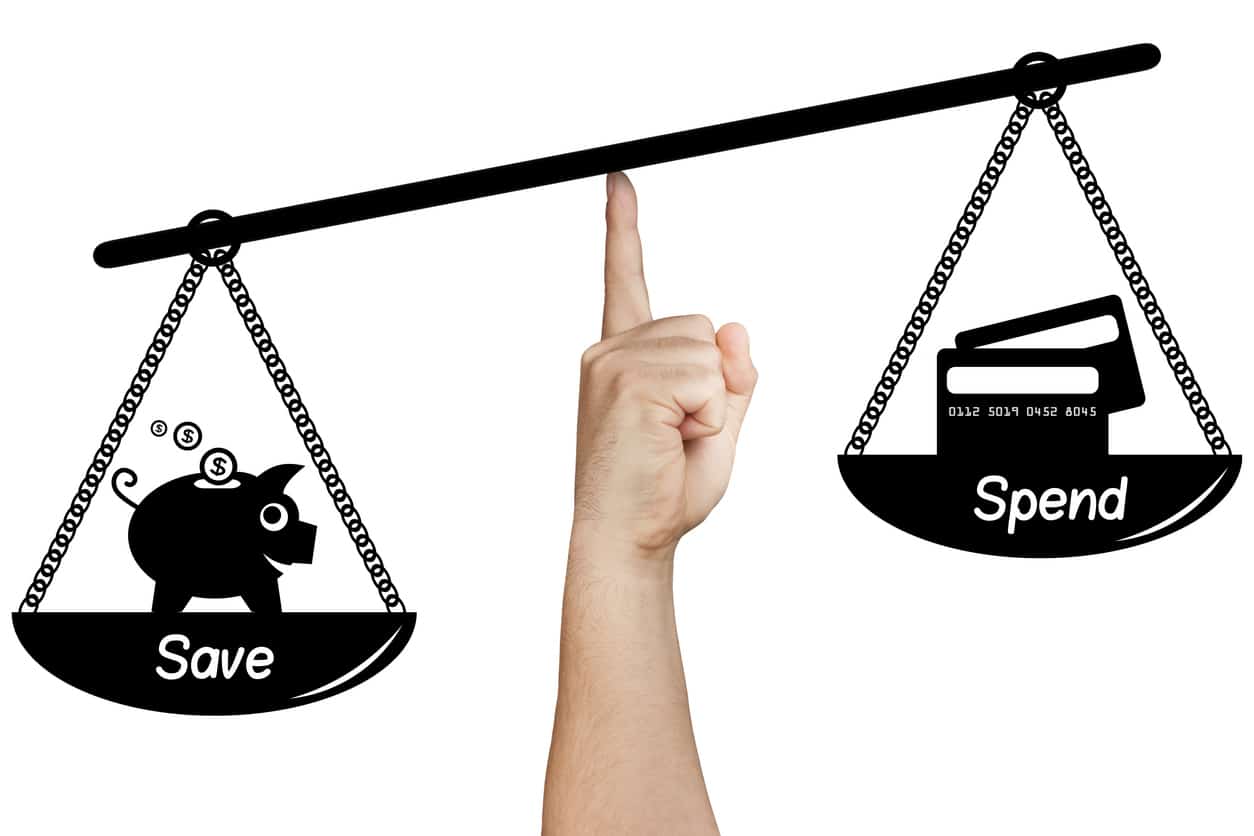

Do you see yourself as a spender or a saver? And is one of them better?

Either way, you’re likely to be wrong.

Most of the language we use around money is unhelpful and usually polarising.

The classic “are you a spender or a saver?” question is a great example of this.

Why?

Because managing your finances over your lifetime involves spending, saving and borrowing.

It’s a triathlon, not a single sport.

Focus too much on one part and you ‘underperform’ on the others.

Where this creates most problems is when people attach their identity to one of the three and that compromises their ability to engage with the other two.

If your identity is a saver, then spending is hard, especially when you get to retirement.

If your identity is a spender, then it becomes harder to build wealth.

If your identity is based on never borrowing money, then you will miss out on investment opportunities.

If you are too attached to borrowing money, then you’re likely to come unstuck at some point.

If you think of spending vs saving as opposite ends of the money spectrum, then that is where you find the extreme money behaviours.

The healthy behaviour is in the middle, but we don’t have a word for it because it involves being able to engage with three separate activities.

We need to save in order to build wealth, as well as a safety cushion.

We need to spend so we can enjoy ourselves and give pleasure to those we care about.

We need to borrow for major purchases and to invest in ourselves.

And the balance between the three will change over your lifetime. So, you definitely need to be able to do all of them.

If you find yourself too attached to spending, saving or borrowing, then contact me to find out how to achieve more balance.

If you’d like to explore how to help your clients who seem stuck, we have a number of CPD approved courses.